The crypto industry has criticized financial regulators in the United Kingdom (UK) for their slow and stringent application approval process, but a blockchain think tank believes good crypto regulations will take time to shape and implement.

Since January 2020, firms carrying out crypto asset activities in the UK must register with The Financial Conduct Authority (FCA). On Aug. 30, international law firm Reed Smith revealed in a Financial Times report the FCA was taking an average of 459 days to process a crypto firm’s registration.

The FCA defended its stance in an Oct. 21 post, arguing that maintaining rigorous standards with crypto regulations is important to protect consumers and preserve the integrity of financial markets.

Speaking to Cryptopolitan, Dr Mureed Hussain, executive director of the British Blockchain Association (BBA), said members of the association had shared concerns about the FCA’s slow process and approach to crypto regulations.

However, he thinks navigating the complex digital asset environment and creating robust crypto regulations is a complex task that takes time to get right.

“Building a well-regulated, innovative, and globally competitive crypto ecosystem takes time,” Hussain said.

“While the industry is moving fast, policies and regulations can sometimes lag. However, there are two ways you can do things: quickly or properly.”

A balance between innovation and ensuring compliance

Since the new rules on crypto asset promotion came into force in the UK in 2023, the FCA has issued application extensions.

Hussain said the FCA has also provided guidance and pre-application meetings with firms, helping them better understand and meet these important requirements.

While it is a step in the right direction, Hussain says the goal should ultimately be a balance of fostering innovation and ensuring compliance with regulations, which is critical to the sustainable growth of the crypto industry.

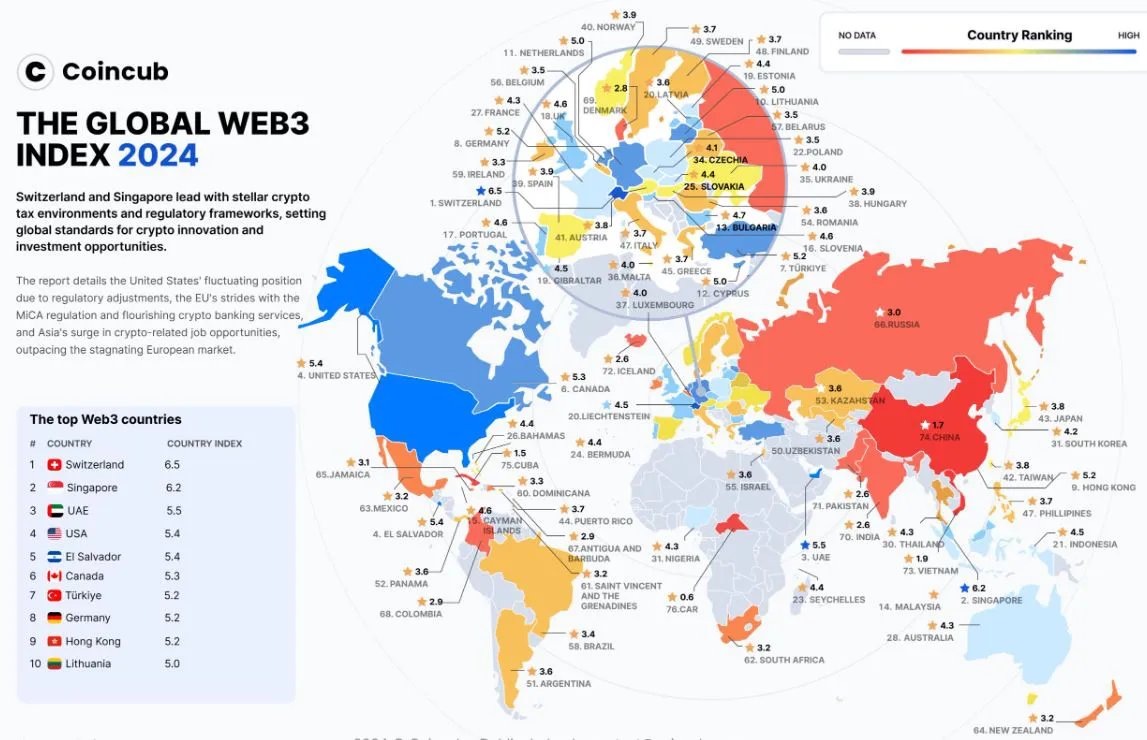

“While we are not yet among the top 10 countries in terms of crypto innovation and leadership, there is significant potential for us to reach the very top,” Hussain said.

According to the Global Web3 Index from the crypto analysis platform, Coincub, Switzerland, Singapore, and the United Arab Emirates are the top three countries for crypto innovations in 2024.

In its methodology, Coincub lists all three countries as having a robust and progressive regulatory framework for digital assets.

Constructive dialogue must continue with crypto regulations

The FCA revealed in its annual report that 87% of crypto registrations in the UK had been withdrawn, rejected, or refused because of “weak” fraud protection and Anti-Money Laundering safeguards.

The FCA’s feedback on “good and poor quality applications ” shows at least 240 applications were withdrawn in the last three years. The number of crypto firms applying for registration has also declined, with only seven firms applying in the first half of 2024, down from 42 in the previous year.

Deborah Cleary, an advisory board member of the BBA, said that going forward, there needs to be ongoing constructive dialogue between regulators, industry participants, and the government to ensure the UK remains a global leader in blockchain and digital assets.

“It is vital to encourage innovation while ensuring robust regulatory standards, enabling both growth and consumer protection,” she said. A thriving and competitive crypto sector must be built on trust and security, Cleary added.

Governments around the world have tried several different approaches to crypto regulation; some have attempted to engage with the industry, others have ignored it, and some have outright banned or tried to shut it down.

Professor Dr. Naseem Naqvi MBE, President of the BBA, said that achieving a UK blockchain revolution might require the country to “think and deliver differently to lead in Web3.”

At the moment, he says the UK has taken “a cautiously optimistic approach.”

“We need to be more dynamic and agile and engage proactively with stakeholders to stay at the forefront of crypto innovation,” he said.

“Industry clarity, support, and guidance are essential. Crypto policies and regulations must be fit for purpose, futuristic, business-friendly, consumer-centered, and based on trustworthy, reliable evidence,” Naqvi added.